Closing the conference, Delphine Lievens, now Head of Distribution at Bohemia Distribution, formerly Senior Box Office Analyst at Gower Street presented a slate of optimism for cinemas. “We’ve still got a way to go,” she began, “but we’re going in the right direction.”

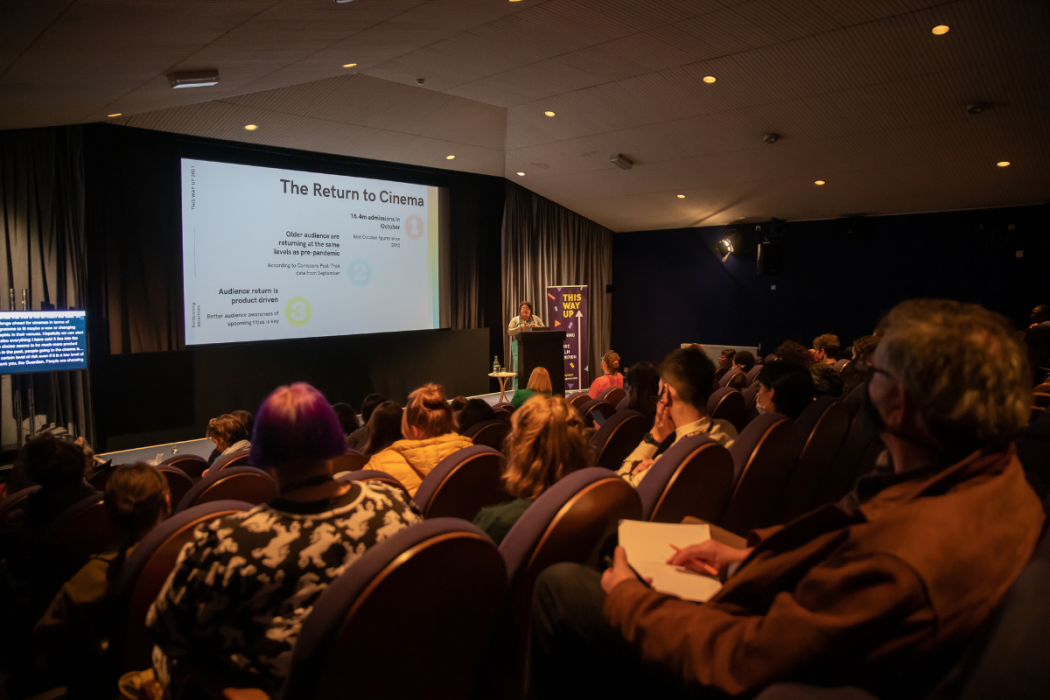

October 2021 cinema admissions were huge, reaching 16.4 million, the highest number since 2012, “October 2012 and October 2021 have something in common,” Lievens admitted, “and that thing is James Bond.” As anticipated, Bond and other blockbusters have been the headliners in sector recovery. Candyman, and Shang Chi – which took 21.3 million at the box office and is currently the third biggest film of the year – have also had a big impact. But can the same be said of independent titles? What does recovery look like for smaller, independent cinemas?

“Indie titles came into their own earlier in the year when there was less Hollywood content for them to compete with,” Lievens said, pointing to the success of Chloé Zhao’s Academy Award winning Nomadland and Thomas Vinterberg’s Another Round. “We’ve now got films where production was delayed,” she continued, “there will be some gaps as the schedule continues to recover.”

Returning Audiences and Trends

A chief concern for many cinemas is older audiences not returning and the summer months skewed to 16-34s. However, Lievens was keen to point out that ComScore are now suggesting that older audiences are returning to the same levels as pre-pandemic and the same is true for all audience groups, according to their surveys. But this data doesn’t count for the small number of people returning and, at least according to discussions with many independent exhibitors, is not true for all cinemas. The challenge ahead, she said, is how to fit to the new or changing demographics in cinemas.

“Audience choice seems to be more product-driven than before,” she revealed, “because it’s a lower risk.” Without the usual levels of attendance, there is a further knock-on effect of audiences interacting less with trailers, point of sale, and other traditional forms of marketing. This means awareness of upcoming releases is lower, and in-venue and social marketing needs greater and concentrated focus.

Lievens went on to identify the following key emerging trends –

- Less mid-range product – the films that did between 1-5 or 1-10 million at the box office. Studios are going for the bigger franchises and it’s harder for distributors to justify the costs to release indie titles.

- A call for more diversity – the continuing conversations and the proof that there are untapped groups in our communities means that, at a time when recovery is so important, it makes sense to broaden your horizons for the audience.

- Hollywood aren’t always the key players – people are watching more foreign language content, including the Korean television series, Squid Game on Netflix (the platform’s most watched series ever with 142 million views); suggesting it’s not always subtitles that are the barrier to audiences. Instead, it’s about marketing and making it feel accessible, not elitist.

- France, Spain, Australia and China – these markets have shown how home-grown content is important to recovery. This highlights our need to nurture home-grown UK film, which will further help futureproof venues to rely less on Hollywood fare.

Upcoming Slate

Lievens went on to highlight a number of quality films (listed below) across a variety of genres and audience appeal. Under the banner of “Diverse Titles”, Lievens stressed that diverse content has a wide appeal, hoping cinemas are “not just putting these films into a niche category because of who they are about.”

- Ailey (Dogwoof, Jan 7th)

- Rebel Dread (Bohemia, March 4th)

- Lingui (Mubi, Feb 4th)

- Boxing Day (Warner Bros, Dec 3rd)

- Easter Sunday (eOne, April 1st)

- Nope (Universal, July 22nd)

- Lola (Peccadillo, Dec 17th)

- Bliss (Bohemia, Dec 24th)

- Great Freedom (MUBI, March 4th)

- Flee (Curzon, Feb 11th)

- Cicada (Peccadillo, Jan 25th)

- Rūrangi (Peccadillo, Feb 22nd)

- Titane (Altitude, Dec 31st)

- Memoria (Sovereign, Jan 14th)

- Belle (National Amusements, Feb 4th)

- Compartment No 6 (Curzon, April 1st)

- Benedetta (MUBI, April 22nd)

- Hit the Road (Picturehouse, June 17th)

- The Duke (Warner Bros, Feb 25th)

- Belfast (Universal, Jan 21st)

- The Phantom of the Open (eOne, April 15th)

- Boiling Point (Vertigo, Dec 30th)

- Ali & Ava (Altitude, Feb 4th)

- The Feast (Picturehouse, April 29th)

Lievens believes things are looking up, and refuses to believe cinema is dead when so many quality films are being produced and distributed, “There are so many more but this is just a sample… and so hopefully it’s true that audiences don’t mind reading subtitles now.”

Image c/o Shamphat Productions